Gazprom & Russian Gas Production Overview & Future Developments Part 2

In part 2, we conclude the article by looking at the production outlook, including market risks. (Click here for Part 1)

Production Outlook

While the discussion above points to considerable upstream activity, much of the expected production increments in the coming years come from either the Nadym-Pur-Tazovsky Region (existing fields still ramping up, particularly the Urengoy fields) and the Yamal peninsula. Both of these projects are already completed or well underway such as Bovanenkovo. As such, the scope for significant project delay is limited.

For the projects that are further out, the scope for further delay is more significant and for the most difficult areas (off-shore Arctic drilling), we expect to see little to no gas supply in the coming ten years. This leaves the Eastern corridor gas projects as the biggest source of potential gas and delay, given the extent and ambition of the project. However, all of this gas is focused on the Asian market and as such, is less important for the European gas market.

Using the ramping profiles provided by Gazprom and our own interpolations, we assume maximum capacity will be reached at the later date in the range, and ramp in a more linear fashion than some of the indications provided by Gazprom. We expect Gazprom will be looking to market, by:

» 2020, some 150 bcm/y of additional gas, with almost all of that coming from the Nadym-Pur-Tazovsky and Yamal regions.

» 2025, there will be some 285 bcm/y of additional gas production. While some gas will be coming from the offshore Arctic, these are small volumes from the Kamennomysskoye fields. We assume no gas in this period from Shtokman.

We note our estimates for incremental new production do not include gas from the Zapolyarnoye field, currently the Russian field with the largest production volume. This field reached its full projected capacity of 130 bcm/y in 2013, after a number of expansions to its original scope, having started production back in 2001.

While new production looks like it is going to put considerable volumes into the market, total production will be influenced by the decline rates at its existing fields. While some of Gazprom’s existing fields are quite mature, including those in the Nadym-Pur-Tazovsky region, those decline rates will have an important impact on exactly how much production growth will be realised. Having said that, fields like Zapolyarnoye are still years away from decline and given its plateau rate is now around a quarter of total Gazprom production, it is helping to largely fill in the decline from the older fields on its own.

Given this, we expect decline from existing producing fields will average out to be between 2-4% per annum, with the higher number a conservative assumption vis-à-vis further production growth. With a decline rate of:

» 2% pa, total production increases by 90 bcm/y by 2020 and 187 bcm/y by 2025. This would take Gazprom production up to 560 bcm/y by 2020, which is below the 650-670 bcm/y targeted by the company. Under our modelling, we expect 650 bcm/y of production to be reached by 2025.

» 4% pa, total production increases by 54 bcm/y by 2020 and 123 bcm/y by 2025.

With either of these assumptions, Gazprom appears to be facing an overhang of gas production capacity that will increase in the future, and this raises question in the context of how and where it markets its gas.

Headwinds: Financing the Expansion

Implicit in these numbers is an assumption there are no delays outside of the ranges provided by Gazprom. While this is a defensible assumption in terms of Yamal projects (Bovanenkovo at least) and the augmenting of the existing producing regions, this is a much larger leap for the eastern gas corridor project.

While we have alluded to the technical issues facing Gazprom (a cold operating environment), we think most of them have already been encountered with the Yamal project. However, adding the greater geological complexity in eastern Siberia compared to the Urals regions, delays are expected.

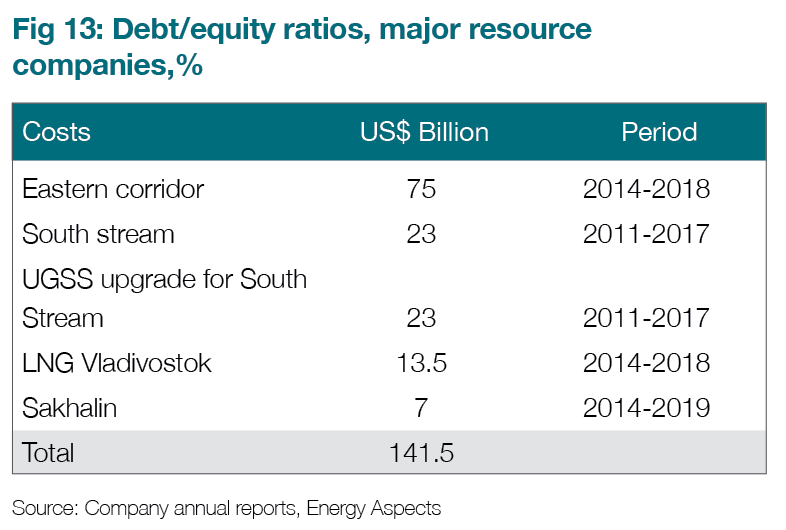

A bigger challenge will be funding so much expansion at one time. The first estimates of the cost of the Eastern corridor are somewhere around the $75 billion level. It was not clear exactly how much of the eastern corridor that is meant to cover, although we expect it would do well to cover the upstream developments in the Yakutia and Irkutsk, and the Power of Siberia pipelines to the Chinese border. Add expected capex for the upgrades to the UGSS and Vladivostok LNG ($14 billion) and further upstream development in the Yamal and Sakhalin, and the capex burden has been built.

Over the last three years, Gazprom capex averaged in the region of $38 billion, and we expect that for the 2014-2018 period, annual capex will likely have been above $40 billion to deliver the major projects to which it is committed. As the cost of development for such large-scale projects will increase during their construction, the current estimates are likely to be on the low side of what Gazprom will need to invest.

Ability to Fund from Earnings

Gazprom funds from its earnings. In 2013, Gazprom reported net profit of the group in 2013 put at $25 billion. With some of the net profit distributed to shareholders, it is clear a continuation of the heavy investments Gazprom is undertaking will have to mean an increase in its debt levels.

Gazprom will also have to manage all of this with the ongoing reduction it sees in the price it is paid for its output. In 2013, Gazprom’s weighted average price of its sales fell by 4% despite wholesale gas prices increasing in Western Europe by 14%. This was due to a sustained programme of contract renegotiation with its main western European customers that lowered contract prices in a year of higher hub prices. With greater hub indexation now in those contracts in some shape or form, Russian gas sales will see further y/y reductions, as hub prices are down by -26% this year. Without any further reform of domestic gas prices, Gazprom will find it increasingly difficult to finance a high proportion of its capital expenditure from its earnings.

Debt Financing: Sanctions

Gazprom has leverage levels at the high end of the major resource extraction companies, with its 2013 debt to equity ratio at 19%. This is possibly due to it having relatively small oil revenues compared to its gas revenues in terms of its peer group.

The US and EU have been enacting progressively tougher sanctions on Russia over 2014 in response to the Ukraine crisis. These sanctions targeted the oil and gas sector, but the intention was not to disrupt current oil and gas exports that represent a significant proportion of European (and global) energy supplies. Instead the sanctions have been designed to impact the long term prospects of the Russian energy sector by restricting access to western financing and technology.

Through July and August sanctions were imposed on a growing list of Russian banks and oil companies. The US sanctioned the gas firm Novatek in July, but Gazprom was notable for its absence from both EU and US sanction lists. This reflected EU concerns that imposing any sanctions on Russia’s largest gas producer, even ones not designed to disrupt current production or exports, could impact European gas markets and wider economies. However, on 12 September, the US added Gazprom to the list of energy companies that face restrictions on dollar lending, for terms of more than 90 days. This is a move that the EU still has not followed, because of supply disruption concerns.

The sanctions will make it more difficult for Gazprom and Novatek to finance debt on international markets. They are formally blocked from working with US companies and individuals, and the indications are that they will find it more challenging to attract buyers on Eurobond markets—even though the EU has not sanctioned the gas companies. The political risks will put many buyers off investing in bonds from Gazprom and those still willing to enter into deals will expect higher returns, raising the costs of borrowing. The financial sanctions will have more effect than the restrictions on technology and services linked to arctic, deepwater and shale projects, as these make up a relatively small portion of Gazprom’s portfolio. The sanctions have also led to the cancellation of the South Stream pipeline project.

Debt Financing: Other

While recourse to western debt markets looks more challenging, there are other sources of financing.

For the Eastern corridor projects, tapping into China’s surplus of funds is likely to be an important source of additional financing. When the 38 bcm gas deal with China was signed earlier in the year, it was reported that Russia will invest $55 billion, while China will invest at least $20 billion. It was reported the $20 billion was for pre-payment for future delivered gas.

As part of the negotiations, Russia reportedly lifted an informal ban on foreign ownership of strategic assets, apparently opening the way for Chinese companies to take part in developing the gas fields and pipeline. This would open the way for some equity holdings in the resources, which would be attractive to China. In addition, reports have surfaced that Russia is looking to Chinese banks for long term debt, and while Chinese banks may want to provide this, they will also be careful not to fall foul of western sanctions.

While we understand Chinese banks are increasingly lending to Russian natural resource companies, lending to sanctioned Russian companies is highly sensitive. Any loans from Chinese banks are likely to be done on a low profile bilateral basis initially, and loans by Chinese banks are likely to be denominated in Renminbi (Rmb) or roubles, as Chinese lenders with large operations in the US will find it difficult to lend dollars in the face of sanctions. Chinese banks are already big lenders to Gazprom and the climate of sanctions is reportedly allowing them to boost business with these clients.

The Russian state also provides support to its oil and gas companies, and as Gazprom is 51% owned by the state, it is likely to benefit from such support. State support tends to be in the form of: provision of goods and services at below market value (historically 50%-75% of subsidy levels); foregone government revenue through a policy of tax rebates and incentives (20%-40%); and direct financial transfers (2%-4%). However, it is challenging to get a handle on how much resource might be available from the Russian government to realise these projects.

The longer the sanctions on Russia hold, the more difficult replacing access to western capital markets. This creates some risk to the timely completion of these projects.

Marketing the Gas: Pricing and Russia’s Relationship with Western Europe

Given our assumptions on production growth, Gazprom is building up a ‘gas bubble’ that suggests it needs expanding markets in order to monetise these investments.

Setting aside Chinese demand that will be met with the Eastern corridor gas, the problem for Gazprom is with its Yamal gas, and where it goes? The answers are not easy. Gazprom has some challenges, as:

» Its main western European market has failed to grow:

–Low economic growth and stagnation in energy intensive industry has meant gas demand has failed to expand in residential, commercial and industrial sectors.

–Low global coal prices and a recession induced softening of carbon prices since 2011 has left gas out of merit in the last few years. With increasing levels of renewable capacity squeezing thermal generation, it will take either a strong reduction in gas prices or an increase in carbon prices to stimulate further demand.

» Its relationship with its EU partners is at a low, as the fallout from the Ukraine crisis is causing a rethink in EU capitals over the current dependency of the block on Russian energy. The deterioration in the relationship is now reflected in the debates over:

–The South Stream pipeline, with Brussels doing what it can to make life difficult for the project, which eventually contributed to the decision to cancel the project and explore an alternative ‘Turk Stream’ route.

– The 2030 energy framework, with greater focus likely to shift back to the promotion of renewables and energy efficiency, two policy topics likely to see more attention, precisely for the impact they could have on fossil fuel demand.

–Potential other supplies for the EU from such ‘desirable’ exporters as Iran (Focus piece: Iran – so far, so close, 6 August 2014).

There is a lack of obvious alternative to a less than welcoming EU market. The Middle East has its own gas and with relationships with Iran normalising, it is better placed to expand its exports into the region. LNG is facing its own global glut, as big volumes of Australian and US gas are due to enter the market by 2020. There is Asia, and expanding gas exports to China would be possible through the western route, which ties up to China’s West-East pipeline system. But the Chinese are difficult negotiators and have their own issues over supply security they want to deal with, which may make further gas sales there just as complex as the first agreement.

This brings us back to Western Europe, which for all of its issues, has a large volume of repressed demand available in the regions underused CCGTs. If gas can get into power, than there is a market, and it becomes just a price issue.

In its production outlook, Gazprom said it was committed to the principle of producing as much gas as demanded, provided there are ‘favourable market conditions’. Gazprom has previously been happy that customers, required to take or pay, would ramp down to annual minimums in the event of insufficient demand. The introduction of hub indexation has changed this somewhat, and with less flexibility in the contracts, nominations this year have been high and this has had a significant impact on hub prices. With Gazprom potentially bringing big volumes of gas to market, the question is does it sit on the bubble and hope the carbon price eventually does the work?

Or does it pop the bubble and go for market volumes over price? These are big questions that Gazprom must grapple with and while time will tell what option they choose, it is hard to expect they will choose

the latter.